Friday, December 28, 2012

Some fascinating research by Ed Lazear, Kathryn Shaw and Christopher Stanton has evaluated the importance of a good boss. They find a substantial effect - a finding that has important implications for both the debate about remuneration of senior bosses and the more general question of how marginal productivity should be measured.

Wednesday, December 05, 2012

The Chancellor of the Exchequer presented his Autumn Statement earlier today. At the time of the last election, the main parties offered economic policies that differed in terms of how quickly they would tackle the budget deficit. The reality is now that the deficit will be closed more slowly than either party planned. This throws into pretty sharp relief the extent to which wiggle room has vanished.

A major difficulty over the last two years has been the continued weakness of the Eurozone. This has hit growth, and consequently had an adverse effect on tax receipts.

Taxpayers know that the deficit must be paid off sometime. The trick is to phase the austerity measures in such a way that, in time, they result in a reduced burden of debt, while not choking off the growth that is essential to the repayment of that debt. Current forecasts suggest that it will be the latter half of next year before any significant growth resumes, and this makes the balancing act particularly difficult. In this context it is particularly important that fiscally neutral changes in tax and government spending should be tilted to favour growth - this means that the raising of tax allowances and the investments in infrastructure are both to be welcomed.

Meanwhile, the statement points to the spending review that is to take place in the first half of 2013. The plans for deficit reduction, and specifically for government spending, in this statement indicate that the review will need to take a draconian stance. The extent to which that turns out to be feasible in practice will depend heavily on the broader macroeconomic context. If the European economy remains fragile beyond 2013, further fiscal retrenchment at home is likely to prolong still further the return to significant levels of growth. Indeed, the extent of retrenchment that is anticipated in today's statement may prove infeasible.

Thursday, November 22, 2012

The latest results from my neural network forecaster for the UK continues to suggest that economic recovery is likely to be consolidated only in the latter part of next year - and the indications are now that the rate of this recovery will be quite slow.

The fragility of the economy in the Eurozone remains a concern - regardless of conditions within the UK itself, there are still some significant downside risks.

Thursday, November 08, 2012

Fiscal Studies has published a special issue on higher education finance, and has made the contents freely avaiable for download. It's a good read. I particularly like the paper by Chowdry et al. Two things in their paper strike me as particularly interesting:

(1) 'The proportion of graduates who reach the new debt write-off point of 30 years increases to 56 per cent' - in other words most graduates will never repay the full amount of their loan. Indeed, 'the average female graduate will pay back just over half of what they borrow, compared with 87 per cent for the average male graduate'. This, of course, means that many (if not most) students are indifferent about the precise level of fees that they are charged, and this in turn incentivises many universities to charge at the cap of £9000. Another implication of this is that the taxpayer ends up having to bear the burden of the unpaid debt, so that the exchequer savings of the new scheme are not as great as might have been hoped. On the assumption that growth raises graduate earnings by 1.5% per year, the exchequer savings amount to £500m per year - which represents a relatively minor reduction in the public sector deficit.

(2) The paper does not produce revised estimates of the rate of return to higher education. It does point out that the average graudate 'will in futre make repayments totalling £25830 over their lifetime - an increase of 52%' compared with the system that existed before 2012. Meanwhile, 'the average student enjoys an increase in cash support during their degree of some 12 per cent, amounting to £19580 in total'. For some students at the margin, the rate of return to higher education has presumably fallen to such an extent that the investment is no longer worthwhile.

Chowdry, H., Dearden, L., Goodman, A., & Jin, W. (2012). The Distributional Impact of the 2012-13 Higher Education Funding Reforms in England* Fiscal Studies, 33 (2), 211-236 DOI: 10.1111/j.1475-5890.2012.00159.x

Thursday, November 01, 2012

The latest World Economic Outlook publication by the International Monetary Fund offers interesting evidence on fiscal multipliers. While 'fiscal multipliers were near 0.5 in advanced economies during the three decades leading up to 2009', the report finds that 'multipliers have actually been in the 0.9 to 1.7 range since the Great Recession'. Simon Wren-Lewis has recently provided a compelling analysis of what this means for the UK. While the global economic environment has done little to help, the double dip may well have been avoidable.

Thursday, October 25, 2012

The 1% increase in GDP achieved in the third quarter of this year represents tremendously welcome news. Part of this increase is surely due to the effect of the Olympics, part to the subdued second quarter (with its glut of public holidays), and it is possible that part could be wiped away as more information comes in and revisions are made to the statistics. Nonetheless, it is difficult to perceive this as anything but an encouraging result. The return to growth has come a little earlier than many (myself included) expected. It does contribute towards an explanation of the encouraging employment figures that were released last week.

There remain uncertainties in the economic environment that suggest that the celebrations need to be tinged with some caution. But Mario Draghi's announcement of the European Central Bank's new stance has been helpful, and interest rate spreads in Spain, Italy and Portugal have fallen markedly - and stayed down. They are still too high for comfort, but the position is markedly more encouraging than it was just 6 weeks ago.

Sunday, September 23, 2012

Paul Gregg and Steve Machin have recently examined the way in which the sensitivity of the real wage to unemployment rates has become stronger over the last decade or so. I have noted this in an earlier blog post, though I would argue that the change slightly predated the 2003 point identified by Gregg and Machin.

Whether, as the economy begins to recover, real wage restraint will continue is moot. If wage pressure returns over the next twelve months or so - before the recovery is consolidated - it may well be the case that interest rate hikes will be needed sooner rather than later in order to prevent a stagflation.

Wednesday, September 12, 2012

Thursday, September 06, 2012

The news that the European Central Bank will pursue outright monetary transactions (OMTs) - purchases of bonds issued by eurozone member countries - as a means of reducing borrowing costs for these countries is very welcome. The conditions under which such transactions will take place remain unclear; the ECB intends to purchase bonds only when it perceives serious distortions to the market, where these distortions are based on what it deems to be unfounded fears. Moreover, the ECB's intervention will be conditional upon the action being part of the European Stability Mechanism, making the availability of such support dependent on countries' compliance with fiscal discipline requirements. This last condition is critical, but the binary nature of any judgement about compliance means that pressure will inevitably come to bear in instances where the judgement is marginal. A better solution would be to offer support on a sliding scale, making support more costly where discipline is weaker. This would effectively be the solution offered by conditional bonds.

Nevertheless, the new initiative is a major step forward. It had been anticipated by the markets - the interest rate spreads for countries such as Spain and Italy had already fallen dramatically over the last day or so. In itself, this is a welcome outcome, though the spreads still have a long way to fall.

Friday, August 24, 2012

Some time ago, I reported on the differences between recent UK and US experience in terms of changes in productivity levels. A similar theme has emerged in recent work by Abigail Hughes and Jumana Saleheen. These authors identify some interesting sectoral patterns. Prior to the financial crisis, productivity growth in the services sector in the UK appeared to be strong; the crisis had an obvious adverse impact on (particularly financial) services, and many of the pre-crisis gains were subsequently lost. There has, since, been a modest recovery in productivity in this sector, however.

Meanwhile, productivity in the energy sector - where North Sea reserves are rapidly being depleted - has declined. In this context, driving the UK towards sustainable productivity growth is likely to be a challenge.

Investment in physical and human capital, and policies to foster innovation are conventional cures for productivity malaise. Business investment requires access to finance and also requires confidence that demand will grow into the future.

Continued uncertainty about the macroeconomic outlook - and especially about the outcome of the Euro crisis - is, in the absence of a quick resolution, likely to continue to frustrate hopes of a speedy return to healthy productivity growth.

Abigail Hughes, & Jumana Saleheen (2012). UK labour productivity since the onset of the crisis - an international and historical perspective Bank of England Quarterly Bulletin, 138-146

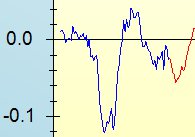

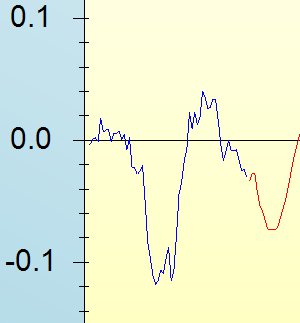

The latest results from my neural network forecasting model, based on industrial production (K222) in the UK are presented below - the data are outturn rates of growth up to June of this year (in blue) and forecasts for the following 24 months (in red).

It is clear that the medium term outlook remains grim. While the growth rate has by now pretty much bottomed out, these data suggest that the return to a positive rate of growth will not come until late next year.

Of course, such a simple model cannot take into account the plethora of uncertainties surrounding the Euro crisis and its ramifications for economic conditions in our major export markets. The risks there, however, remain predominantly on the downside.

The public finance data for July were disappointing; a prolonged recession is likely to mean dampened government revenues and increased government spending on welfare, so, while output struggles to recover, the outlook for deficit reduction is poor.

Tuesday, July 24, 2012

As I wrote last month, the news from Spain provides a cold shower. The recent movement of the spread showing the difference between interest rates at which the Spanish authorities can access debt and the German counterpart has been alarming. With the spread now well over 6 per cent, Spain's debt is becoming unsustainable, and a bail-out is looking increasingly inevitable.

A rescue package for an economy the size of Spain's will inevitably put strain on other European economies. With this scenario as the backdrop, the news that Moody's credit rating agency has announced negative outlooks for Germany, the Netherlands and Luxembourg, is unsurprising.

A rescue package for an economy the size of Spain's will inevitably put strain on other European economies. With this scenario as the backdrop, the news that Moody's credit rating agency has announced negative outlooks for Germany, the Netherlands and Luxembourg, is unsurprising.

Monday, July 09, 2012

News that BPP, the for-profit university college, is launching cut-price degrees in nursing and psychology comes side by side with some warnings from economists who have studied the for-profit higher education sector in the United States. Kevin Lang and Russell Weinstein find that, while the returns to studying for a degree from a traditional insititution of higher education are considerable, those associated with degrees (and other qualifications) from for-profits are negligible. Similar observations have been made by Nobel prizewinner Joe Stiglitz. As the UK for-profit higher education sector branches out into health, prospective students receive a health warning about such ventures.

Wednesday, June 20, 2012

The contrasting experiences of the UK and US over recent years, in terms of changes in labour productivity, has been noted for a while. Now, Abigail Hughes and Jumana Saleheen have produced an analysis that shows that UK productivity - having grown strongly in the run-up to the Great Recession - has been sluggish since, in comparison not only with the US but also with other major European economies.

The relatively strong productivity growth in some other economies - particularly in southern Europe - may well be due to the rapid increase in unemployment, with relatively low productivity workers losing their jobs. But the sluggish growth productivity in the UK has to be a source of concern. It reflects, in part at least, a lack of confidence in future prospects, and a consequent failure of businesses to invest.

While demand factors likely dominate the economic situation in the short term, in the longer term supply factors are clearly of paramount importance. The supply side issues that underpin the underperformance of the UK in international comparisons of productivity therefore warrant urgent attention.

Abigail Hughes and Jumana Saleheen (2012). UK labour productivity since the onset of the crisis — an international and historical perspective Bank of England Quarterly Bulletin, 52 (2), 138-146

The relatively strong productivity growth in some other economies - particularly in southern Europe - may well be due to the rapid increase in unemployment, with relatively low productivity workers losing their jobs. But the sluggish growth productivity in the UK has to be a source of concern. It reflects, in part at least, a lack of confidence in future prospects, and a consequent failure of businesses to invest.

While demand factors likely dominate the economic situation in the short term, in the longer term supply factors are clearly of paramount importance. The supply side issues that underpin the underperformance of the UK in international comparisons of productivity therefore warrant urgent attention.

Abigail Hughes and Jumana Saleheen (2012). UK labour productivity since the onset of the crisis — an international and historical perspective Bank of England Quarterly Bulletin, 52 (2), 138-146

Much of the debate about the merits of austerity policies concerns an empirical issue: how effective can fiscal policy be in stimulating the growth that can later help pay off deficits? Some new evidence on this comes from a paper by Karel Mertens and Morten Ravn (nicely summarised here). It suggests that the medium term response of national output (around 2 years after a shock) to a change in the tax take is quite substantial. Over the long run, of course, it is real things (such as productivity) that affect output growth - but over the short and medium term, fiscal policy can give the economy a substantial kick.

Arguing in favour of a fiscal injection that would, in the short term, serve to widen the government's budget deficit does of course represent a tough political challenge. But the evidence is clear that such an injection would serve to promote growth. And, with inflation now back within the Bank of England's target range, the argument that it would stoke inflation is increasingly difficult to sustain.

Karel Mertens and Morten Ravn (2012). A reconciliation of SVAR and narrative estimators of tax multipliers Cornell University Working Paper

Arguing in favour of a fiscal injection that would, in the short term, serve to widen the government's budget deficit does of course represent a tough political challenge. But the evidence is clear that such an injection would serve to promote growth. And, with inflation now back within the Bank of England's target range, the argument that it would stoke inflation is increasingly difficult to sustain.

Karel Mertens and Morten Ravn (2012). A reconciliation of SVAR and narrative estimators of tax multipliers Cornell University Working Paper

Monday, June 18, 2012

Friday, June 15, 2012

Two new packages of support for the UK economy have been announced in a speech by the Chancellor of the Exchequer at the Mansion House speech yesterday. The Bank of England's 'funding for lending' scheme will release £80 billion worth of loans, at low rates of interest, to commercial banks which will then undertake to lend to businesses. Meanwhile, in addition, 6-month loans will be offered to the commercial banks - the intention is to loan out at least £5 billion per month in this way. The aim of these two schemes is to effect a significant injection into the economy, which is facing what Mervyn King, Governor of the Bank of England, yesterday described as 'an ugly picture'.

Faced by such a dismal economic picture, the success of these initiatives will depend on the extent to which extra liquidity will translate into extra economic activity. With gloomy prospects and low levels of confidence about the medium term outlook, businesses may not consider this to be the best time to invest. Pushing 'Plan A' - expansionary monetary policy combined with fiscal retrenchment - to the limit is all well and good. But in a liquidity trap monetary policy alone cannot deliver growth.

Faced by such a dismal economic picture, the success of these initiatives will depend on the extent to which extra liquidity will translate into extra economic activity. With gloomy prospects and low levels of confidence about the medium term outlook, businesses may not consider this to be the best time to invest. Pushing 'Plan A' - expansionary monetary policy combined with fiscal retrenchment - to the limit is all well and good. But in a liquidity trap monetary policy alone cannot deliver growth.

The government's White Paper on banking reform, published yesterday, represents a response to the report of the Independent Commission on Banking led by Sir John Vickers. The recommendations made by Vickers have in large measure been taken up. This means that retail banking will be ring-fenced, protecting depositors in the retail market from potential adverse consequences of risky activities undertaken elsewhere in the bank. Vickers (in paragraph 2.28 of the report) recommended that the leverage ratio (the ratio of equity to assets) should be set at a minimum of just over 4% for large banks - above the international norm of 3% - as a means of safeguarding the ring-fenced activity against excessive risk. The White Paper indicates that the government has not accepted this recommendation, and retains a 3% requirement. Nevertheless, the government's proposals are, in large measure, those of the Commission.

Much remains to be done, however. A key failing of the banking system is that it is insufficiently competitive. The players in this industry are too large. Given the extent to which economies of scale prevail, it is easy to understand how this situation has come about. Nonetheless, other industries are subject to regulation to ensure competition, and banking needs to be no different. The White Paper makes reference to the forthcoming divestment of part of Lloyds Banking Group, and points out that this is an opportunity to increase competition. It is indeed such an opportunity, but I suspect that, beyond hoping that this will be so, the need for much more aggressive regulation remains acute.

Much remains to be done, however. A key failing of the banking system is that it is insufficiently competitive. The players in this industry are too large. Given the extent to which economies of scale prevail, it is easy to understand how this situation has come about. Nonetheless, other industries are subject to regulation to ensure competition, and banking needs to be no different. The White Paper makes reference to the forthcoming divestment of part of Lloyds Banking Group, and points out that this is an opportunity to increase competition. It is indeed such an opportunity, but I suspect that, beyond hoping that this will be so, the need for much more aggressive regulation remains acute.

Monday, June 11, 2012

Spain has become the latest country to require a support package. The EU will provide loans worth up to 100 billion to support the Spanish banking system, this being offered at terms favourable to the Spanish government. Spain's banks performed poorly last year in stress tests conducted in 2011 by the Committee of European Banking Supervisors, and have been left particularly vulnerable following the bad debts that led to the original credit crunch in 2007-08. The EU loans are intended to support these banks for a period. It may be regarded as another attempt to 'kick the can down the road' - in the hope that by buying time the threat of catastrophic failure can be averted.

The initial response of the markets has not been particularly favourable. The spread between Spanish and German interest rates on 10 year loans has once again widened to above 5 percentage points, after falling over the last 10 days. The spread for Italy, widely seen as being the next country to be affected by this contagion, has also risen - in this case passing through the 4.5 percentage point mark. The key test will be the next bond auctions in Spain, scheduled to take place next week.

The initial response of the markets has not been particularly favourable. The spread between Spanish and German interest rates on 10 year loans has once again widened to above 5 percentage points, after falling over the last 10 days. The spread for Italy, widely seen as being the next country to be affected by this contagion, has also risen - in this case passing through the 4.5 percentage point mark. The key test will be the next bond auctions in Spain, scheduled to take place next week.

Friday, April 27, 2012

The last week has seen the publication of further evidence about the state of the UK economy. First came some promising data on sales, the headline figure suggesting an increase of 1.8% in sales during March. To some extent this was aided by freak conditions - as people brought forward their consumption of fuel at the end of the month owing to fears of a strike by petrol tanker drivers. But retail sales excluding automotive fuel rose by 1.5% over the course of the month, suggesting that relatively little of the growth was due to the unusual circumstances.

Next came the GDP figures for the first quarter of this year. These indicate that the economy slipped back into recession, with negative growth being observed for the second successive quarter. The overall growth rate in the first quarter was -0.2%, but this figure tends to conceal experience that differs quite markedly across industries. The construction sector, in particular, performed badly, with a growth rate of -3.0% in the first quarter. Services (which comprise a high proportion of total output in the economy) grew, but by only 0.1%. So the news on GDP has been very disappointing (albeit not surprising to readers of this blog).

More encouraging news has come in the form of a boost to consumer confidence, with the Nationwide reporting a marked jump in its indicator.

Yet, while the first quarter of this year has been one in which there are a few (very patchy) signs of life in the economy, the wider environment remains one in which there are many uncertainties and downside risks. Spain has become a renewed source of concern - the spread between Spanish and German interest rates increased in early April and shows no sign of coming down any time soon - this spread currently stands at more than 4 percentage points. At the beginning of March it was 3, and at the end of March it was 3.5. Meanwhile, the unemployment rate in Spain has risen to more than 24%, presenting a severe challenge to government policy and raising questions about the sustainability of the country's debt - which is already approaching 80% of GDP. Parallels with Greece are starting to be drawn - but Spain's economy is much bigger than that of Greece, and its difficulties are likely therefore to have larger ramifications elsewhere.

The overall position therefore remains one that is best described as gloomy.

Monday, March 19, 2012

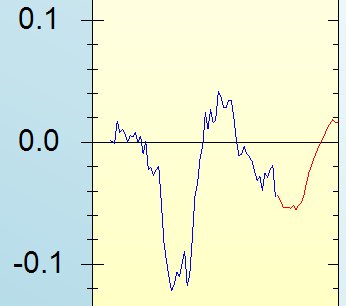

It is a while since I have updated the forecasts produced by my neural network model for the UK. Over the last few weeks, a number of indicators have suggested that there are increasing grounds for confidence.

The forecasts produced by my model do not back this up - indeed they suggest that we may need to wait till the first half of 2013 before we see growth re-establishing itself. After a slight upward blip (round about now), the model predicts that the rate of growth of output will dip back down. Once growth resumes, it rises quite sharply to around 2% per year.

The forecast is, of course, based only on limited information - about industrial output. It is not sophisticated enough to include information about policy shocks - changes in the behaviour of the European Central Bank, the successful Greek debt renegotiation, and so on. It therefore looks, to me, to be a pessimistic forecast. But it may serve, if nothing else, to remind us that times are still uncertain, and there remain some serious downside risks.

The forecasts produced by my model do not back this up - indeed they suggest that we may need to wait till the first half of 2013 before we see growth re-establishing itself. After a slight upward blip (round about now), the model predicts that the rate of growth of output will dip back down. Once growth resumes, it rises quite sharply to around 2% per year.

The forecast is, of course, based only on limited information - about industrial output. It is not sophisticated enough to include information about policy shocks - changes in the behaviour of the European Central Bank, the successful Greek debt renegotiation, and so on. It therefore looks, to me, to be a pessimistic forecast. But it may serve, if nothing else, to remind us that times are still uncertain, and there remain some serious downside risks.

Wednesday, February 29, 2012

In the run up to the budget, there is much interest in the top 50% rate of income tax. Some commentators argue for retaining this band, while others would like to scrap it – the latter group claiming that such a high rate of tax carries the risk that high income entrepreneurs will choose to leave the country rather than pay the tax.

Some evidence on this issue comes from the work of Mathias Trabandt and Harald Uhlig, who calculate ‘Laffer curves’ for a variety of countries. Laffer curves plot tax revenues against the tax rate. Tax revenues are low when the tax rate is low for obvious reasons; they are also low when the tax rate is high because there is then a strong disincentive effect. The Laffer curve therefore takes on an inverse U shape, low at the extremes and peaking at some non-extreme rate of tax. For the UK the Laffer curve peaks at an income tax rate somewhere between 50 and 60 per cent. This suggests that the current top rate is about right.

Some evidence on this issue comes from the work of Mathias Trabandt and Harald Uhlig, who calculate ‘Laffer curves’ for a variety of countries. Laffer curves plot tax revenues against the tax rate. Tax revenues are low when the tax rate is low for obvious reasons; they are also low when the tax rate is high because there is then a strong disincentive effect. The Laffer curve therefore takes on an inverse U shape, low at the extremes and peaking at some non-extreme rate of tax. For the UK the Laffer curve peaks at an income tax rate somewhere between 50 and 60 per cent. This suggests that the current top rate is about right.

Tuesday, February 21, 2012

Results that are apparently strong emerge from simple models of the economy such as those that appear in the textbooks used by our students. In reality, the world is rarely as simple as these models might suggest. More complex models often generate more complex results - in other words, things are rarely so simple as they appear.

The current generation of macroeconomic models is based on building blocks of utility maximising individuals and profit maximising firms, all with the ability to make sensible forecasts of the future evolution of the economy and with the ability to adjust their behaviour in line with the current and expected future economic environment - which includes, amongst other things, government policy. There is a lot going on in these models - just as there is a lot going on in the real world. In many cases, the results obtained from these models are the same as those that emerge from the textbook models. In some cases - unusual cases, perhaps - they are not. Since we live in unusual times, it is not altogether ludicrous to consider some of these unusual cases.

A recent paper does just that. It asks the question: in a world where sovreign debt is approaching the limits of sustainability, does fiscal policy work in the same way as textbook models say it should? The answer is: it may do, it may not. Under certain (extreme) circumstances it may even be the case that austerity can stimulate the economy. Under more plausible scenarios, however, the results of the paper emphasise the 'benefit of delaying fiscal adjustment until after the economy has recovered from the worst of the initial recession'

Giancarlo Corsetti, Keith Kuester, Andre Meier and Gernot J. Mueller (2012). Sovreign risk, fiscal policy, and macroeconomic stability International Monetary Fund Working Paper

The current generation of macroeconomic models is based on building blocks of utility maximising individuals and profit maximising firms, all with the ability to make sensible forecasts of the future evolution of the economy and with the ability to adjust their behaviour in line with the current and expected future economic environment - which includes, amongst other things, government policy. There is a lot going on in these models - just as there is a lot going on in the real world. In many cases, the results obtained from these models are the same as those that emerge from the textbook models. In some cases - unusual cases, perhaps - they are not. Since we live in unusual times, it is not altogether ludicrous to consider some of these unusual cases.

A recent paper does just that. It asks the question: in a world where sovreign debt is approaching the limits of sustainability, does fiscal policy work in the same way as textbook models say it should? The answer is: it may do, it may not. Under certain (extreme) circumstances it may even be the case that austerity can stimulate the economy. Under more plausible scenarios, however, the results of the paper emphasise the 'benefit of delaying fiscal adjustment until after the economy has recovered from the worst of the initial recession'

Giancarlo Corsetti, Keith Kuester, Andre Meier and Gernot J. Mueller (2012). Sovreign risk, fiscal policy, and macroeconomic stability International Monetary Fund Working Paper

Thursday, February 16, 2012

The operations of the European Central Bank since December have helped stabilise what had, until then, looked an increasingly precarious state in the financial sector. Spreads (measuring the difference between the interest rate that a country needs to pay on debt and that which Germany needs to pay) had, until December, risen in a number of European countries and were reaching disturbing levels. The spreads are still high for Greece, of course, and are still high in Portugal (though it recently dipped below 10 after hitting a high of over 15). In Spain, the spread has fallen from over 4.5 to around 3.5; in Italy from about 5.5 to 3.8; and in France from around 2 to around 1.1. Moreover, in the UK, the LIBOR - often seen as an indicator of how confident banks are in lending to one another - has started to fall, thus suggesting that some confidence is being restored in the system - though it still remains more than half a percentage point above the central bank's rate of interest.

Meanwhile, consumer confidence has started to rise.

It remains far too early to suggest that a corner has been turned. Future developments in Europe remain unclear. While monetary policy, with renewed quantitative easing, is likely to stimulate the UK's economy, fiscal policy is still restricting growth. And the labour market situation remains bleak; unemployment typically rises for some time after output starts to recover. But, while still very fragile, the overall economic outlook now looks more promising than has been the case for some time.

Meanwhile, consumer confidence has started to rise.

It remains far too early to suggest that a corner has been turned. Future developments in Europe remain unclear. While monetary policy, with renewed quantitative easing, is likely to stimulate the UK's economy, fiscal policy is still restricting growth. And the labour market situation remains bleak; unemployment typically rises for some time after output starts to recover. But, while still very fragile, the overall economic outlook now looks more promising than has been the case for some time.

Wednesday, January 25, 2012

The UK's output fell by 0.2% in the last quarter of 2011. This is no surprise - some observers have been predicting a fourth quarter fall in output for over 18 months now. That being the case, the policy response has been disappointing. But perhaps that is, in part at least, because official forecasters - such as the Office for Budget Responsibility - got their forecasts wrong. The predictions made by these bodies do indeed impact on policy, and the question needs to be asked: why did these forecasters fail to predict a downturn that was both predictable and predicted?

Tuesday, January 24, 2012

The International Monetary Fund now predicts the Euro area to go into recession this year. It is predicting growth of 0.6% for the UK - this may or may not mean recession in the early part of the year. The Fund anticipates that 'adverse spillovers from the euro area' will stall growth in a wider range of countries, and that the 'downside risks have risen sharply'. Crucially, the Fund states that countries 'with very low interest rates or other factors that create adequate fiscal space, including some in the euro area, should reconsider the pace of near-term fiscal consolidation'. The meaning of 'fiscal space' is discussed in a blog post by Jonathan Portes. The implications for UK policy are clear.

It's taken the IMF a while to get it - but they have not been alone in the policy-making community. Hopefully their words will not fall on deaf ears.

It's taken the IMF a while to get it - but they have not been alone in the policy-making community. Hopefully their words will not fall on deaf ears.

Thursday, January 19, 2012

There have been mixed signals about the economy of late, but consumer confidence remains low. Developments in Europe - with continued uncertainty about the Greek bailout and the future of the euro - combined with further evidence that banks are once again reluctant to lend (with a high and rising LIBOR) render the macroeconomic environment fragile. Meanwhile, the dampening effect of austerity measures on growth has become increasingly evident. A further burst of quantitative easing should be expected in the spring - though that may well come too late to prevent the UK from slipping back into recession.

Youth unemployment is a problem of increasing concern - over a million youths (between the ages of 16 and 24) are now unemployed in the UK; the youth unemployment rate is 22%, well above the overall unemployment rate of 8.6%. The trajectory is up.

The willingness of employers to hire labour is, of course, determined in large measure by its cost. Youth wages have risen by less than adult wages over the last 15 years, so it is not immediately obvious that this is the source of the problem. The elasticity of the real youth wage with respect to the youth unemployment rate is negative (as we would expect) at around -0.1, indicating that a change in the youth unemployment rate from (say) 10 to 11 per cent would bring about a 10 per cent fall in youth wages. That should help to make young people more attractive to employers. Meanwhile, the elasticity of youth wages with respect to the adult wage is high (at a little over 0.8).

Weakening the link between youth wages and adult wages - making youth wages more responsive to conditions in the labour market specifically for young people - might, over the longer term, help alleviate the difficulties that many young people experience in finding work. Of more immediate concern, many firms lack the confidence to invest in new projects that would expand employment, and, where they do wish to invest, they still often lack the access to finance.

The willingness of employers to hire labour is, of course, determined in large measure by its cost. Youth wages have risen by less than adult wages over the last 15 years, so it is not immediately obvious that this is the source of the problem. The elasticity of the real youth wage with respect to the youth unemployment rate is negative (as we would expect) at around -0.1, indicating that a change in the youth unemployment rate from (say) 10 to 11 per cent would bring about a 10 per cent fall in youth wages. That should help to make young people more attractive to employers. Meanwhile, the elasticity of youth wages with respect to the adult wage is high (at a little over 0.8).

Weakening the link between youth wages and adult wages - making youth wages more responsive to conditions in the labour market specifically for young people - might, over the longer term, help alleviate the difficulties that many young people experience in finding work. Of more immediate concern, many firms lack the confidence to invest in new projects that would expand employment, and, where they do wish to invest, they still often lack the access to finance.

Tuesday, January 17, 2012

Some more evidence on what makes schools effective comes from Will Dobbie and Roland Fryer. They find that a mix of policies - including setting clear and high expectations, obtaining regular feedback on teachers, making data-based decisions on pedagogical issues - explain a substantial part of the differences in performance across schools. In light of the work that I reported in a recent blog entry, it is clear that there is a very durable impact associated with high quality schooling. The policies suggested by Dobbie and Fryer are therefore worthy of serious consideration.

Tuesday, January 10, 2012

Recent work by Raj Chetty, John Friedman and Jonah Rockoff suggests that teacher quality has a very considerable impact on students' outcomes - not just in terms of test scores but also in terms of lifetime earnings. These findings have obvious policy implications, but the fact remains that we still know remarkably little about how to create a good teacher. Dan Goldhaber and Emily Anthony provide some evidence that suggests that the characteristics of high quality teachers can be identified - but it is not clear that all of these characteristics can be delivered through training programmes. Based on what we do know, however, Rick Hanushek and Steven Rivkin suggest that an appropriate response is to tighten up on the subject-specific qualifications that are required of teachers, and simultaneously to firm up on human resource management - in particular tightening promotion and retention criteria. In light of the new evidence on the returns to high quality teaching, the societal benefits of such an approach are likely to be substantial.

Goldhaber, D., & Anthony, E. (2007). Can Teacher Quality Be Effectively Assessed? National Board Certification as a Signal of Effective Teaching Review of Economics and Statistics, 89 (1), 134-150 DOI: 10.1162/rest.89.1.134

Goldhaber, D., & Anthony, E. (2007). Can Teacher Quality Be Effectively Assessed? National Board Certification as a Signal of Effective Teaching Review of Economics and Statistics, 89 (1), 134-150 DOI: 10.1162/rest.89.1.134

Thursday, January 05, 2012

Recent research by David Deming, Claudia Goldin and Larry Katz should provide a reality check for those keen on promoting the development of for-profit higher education in the UK. Using data from the US - where for-profits are now a significant player - the authors find that graduates of such institutions are more prone to unemployment and have lower earnings than those from more traditional universities. Moreover - and surely of immediate concern to government - graduates from the for-profit sector face much more severe problems of debt and their default rates on student loans are particularly high.

This evidence is particularly interesting in the context of yesterday's speech by David Willetts, Minister of State for Universities and Science, in which the goal of 'inviting proposals for a new type of university with a focus on science and technology ... (with) ... no additional government funding' was announced. There is, surely, a role to be played by the private sector in higher education. The case in favour of for-profits is not so clear.

This evidence is particularly interesting in the context of yesterday's speech by David Willetts, Minister of State for Universities and Science, in which the goal of 'inviting proposals for a new type of university with a focus on science and technology ... (with) ... no additional government funding' was announced. There is, surely, a role to be played by the private sector in higher education. The case in favour of for-profits is not so clear.

Subscribe to:

Posts (Atom)